Introduction

Filing an Income Tax Return (ITR) is an essential responsibility for every eligible taxpayer in India. It helps you report your income, calculate your tax liability, claim eligible deductions, receive refunds, and remain compliant with the Income-tax Act. While filing an ITR has become much easier through the online Income Tax e-Filing portal, mistakes can still happen.

Many taxpayers realize after submitting their return that they forgot to report some income, entered incorrect bank details, claimed the wrong deduction, or made other errors. This often leads to a common question:

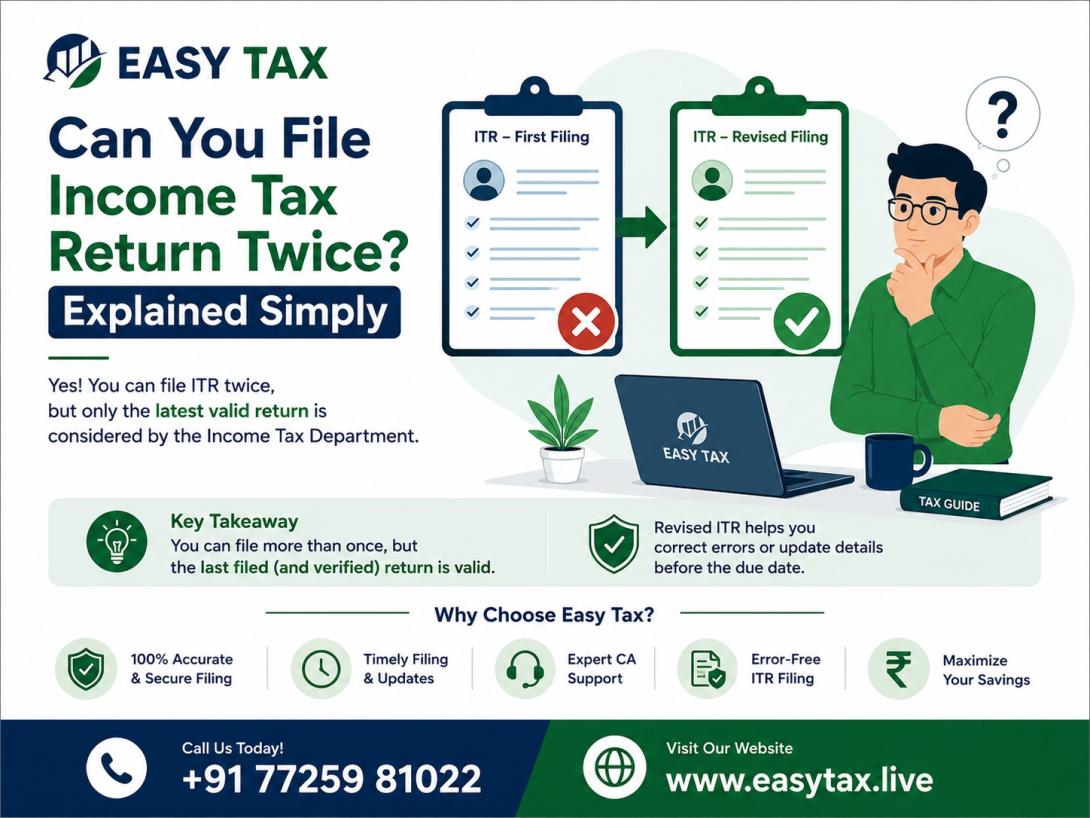

"Can I file my Income Tax Return twice?"

The simple answer is No—you cannot file two original Income Tax Returns for the same Assessment Year. However, the Income-tax Act provides legal options to correct mistakes through a Revised Return or, in certain cases, an Updated Return (ITR-U).

Understanding the difference between these options is important because filing the wrong return or ignoring an error may result in notices from the Income Tax Department, additional tax liability, interest, or penalties.

In this guide, we'll explain when you can modify an already filed return, the circumstances in which a revised return is allowed, and what steps you should take if you discover an error after filing.

Can You File an Income Tax Return Twice?

The answer is No. Once you have successfully submitted your original Income Tax Return for a particular Assessment Year, you cannot file another original return for the same year.

The Income Tax Department accepts only one original return for each taxpayer and Assessment Year. Attempting to file another original return can create inconsistencies in your tax records and may lead to processing issues.

However, this does not mean you cannot correct mistakes. If you identify an error after filing, the Income-tax Act allows eligible taxpayers to file a Revised Return or an Updated Return (ITR-U), depending on the situation.

Therefore, instead of filing another original return, you should use the appropriate correction mechanism available under the law.

Why Do Taxpayers Want to File Their ITR Again?

It is quite common for taxpayers to notice mistakes after submitting their return. In many cases, these errors are genuine and can be corrected if acted upon within the prescribed time.

Some of the most common reasons include:

1. Forgetting to Report Income

A taxpayer may accidentally omit certain sources of income, such as:

- Bank interest

- Fixed deposit interest

- Freelance income

- Rental income

- Dividend income

- Capital gains from shares or mutual funds

Even if the omitted amount appears small, it should be reported correctly to avoid future notices.

2. Incorrect Personal Information

Sometimes taxpayers enter incorrect details while filing, such as:

- Wrong bank account number

- Incorrect IFSC code

- Misspelled name

- Wrong address

- Incorrect email or mobile number

Although some profile details can be updated separately, errors affecting the return itself may require correction.

3. Missing Tax Deductions

Many taxpayers later realize they forgot to claim deductions for eligible investments or expenses.

Examples include:

- Eligible retirement-related deductions

- Education loan interest

- Home loan interest (where applicable)

- Health insurance premium

- Donations qualifying for tax benefits

Missing eligible deductions may result in paying more tax than necessary.

4. Incorrect Tax Calculation

Manual data entry or misunderstanding tax provisions may lead to incorrect tax computation.

Examples include:

- Wrong taxable income

- Incorrect surcharge calculation

- Incorrect rebate calculation

- Errors in tax payments

Correcting these mistakes ensures accurate tax liability.

5. Additional Financial Information Becomes Available

Sometimes taxpayers receive important tax-related information only after filing the return.

Examples include:

- Updated Form 16

- Corrected TDS certificate

- Revised AIS information

- Additional bank interest certificate

If this information affects taxable income, the return may need revision.

6. Wrong ITR Form

Choosing the wrong Income Tax Return form is another common mistake.

For example:

- Filing ITR-1 instead of ITR-2

- Filing ITR-4 despite being ineligible

Using an incorrect ITR form may lead to defective return notices.

7. Reporting Errors in Capital Gains

Investors often make mistakes while reporting:

- Share transactions

- Mutual fund sales

- Property sales

Incorrect capital gains reporting can significantly affect tax liability.

8. Employer Issued Corrected Salary Details

Sometimes employers revise salary information after issuing Form 16.

This may happen due to:

- Bonus adjustments

- Revised TDS

- Salary arrears

- Payroll corrections

Taxpayers should update their return if these changes affect taxable income.

What Should You Do Instead of Filing Another Return?

If you've already filed your Income Tax Return and later discover a mistake, do not attempt to file another original return.

Instead, choose the appropriate correction option provided under the Income-tax Act:

- File a Revised Return if you're eligible and the correction falls within the permitted timeline.

- File an Updated Return (ITR-U) in situations where a revised return is not available but the law allows you to update your return, subject to specified conditions.

Selecting the correct option ensures your tax records remain accurate and compliant.

What Is a Revised Return?

A Revised Return allows a taxpayer to correct mistakes in an Income Tax Return that has already been filed.

It is specifically meant for situations where the original return contains omissions or incorrect information.

Typical reasons for filing a revised return include:

- Incorrect income details

- Missing deductions

- Incorrect tax calculations

- Wrong bank details

- Wrong ITR form

- Omitted financial transactions

A revised return replaces the earlier filed return once it is successfully processed.

When Can You File a Revised Return?

You may file a revised return if you discover an omission or mistake after filing your original return and the applicable legal conditions are satisfied.

A revised return can generally be filed for:

- Incorrect reporting of income

- Missing eligible deductions

- Wrong tax calculations

- Incorrect personal details affecting the return

- Errors in financial disclosures

The correction should be made as early as possible after identifying the mistake.

Practical Example

Suppose Rahul, a salaried employee, filed his Income Tax Return in July.

A week later, he remembered that he had earned interest from a fixed deposit, but forgot to include it while filing.

Can Rahul submit another original Income Tax Return?

No.

Instead, Rahul should correct the mistake by filing a Revised Return, adding the omitted interest income and paying any additional tax, if applicable.

This ensures his tax records remain accurate and reduces the possibility of receiving a notice from the Income Tax Department.

Common Situations Where a Revised Return May Be Needed

A revised return is often filed in situations such as:

- Forgot to report bank interest.

- Missed dividend income.

- Entered incorrect TDS details.

- Claimed an incorrect deduction.

- Reported incorrect capital gains.

- Selected the wrong ITR form.

- Entered incorrect taxable income.

- Forgot to disclose another source of income.

- Incorrect tax payment details.

- Wrong bank account selected for refund.

Identifying and correcting these mistakes promptly helps ensure compliance and avoids unnecessary complications.

Benefits of Correcting Mistakes Early

Correcting errors as soon as they are discovered offers several advantages:

- Improves the accuracy of your Income Tax Return.

- Reduces the likelihood of notices from the Income Tax Department.

- Ensures correct tax liability is reported.

- Helps avoid disputes arising from omitted income.

- Facilitates smoother processing of tax refunds.

- Keeps your tax records consistent and compliant.

Reviewing your return carefully before submission remains the best way to minimize errors, but the availability of correction mechanisms provides taxpayers with an opportunity to rectify genuine mistakes.

What Is a Belated Return?

A Belated Return is an Income Tax Return filed after the original due date but within the time limit prescribed under the Income-tax Act. It provides taxpayers with an opportunity to meet their compliance obligations even if they miss the initial filing deadline.

However, filing a belated return may have certain consequences, such as the payment of applicable interest, late filing fees, or restrictions on carrying forward specific losses, depending on the provisions of the Income-tax Act.

If you miss the original due date, filing a belated return is generally better than not filing your return at all.

What Is an Updated Return (ITR-U)?

The Updated Return (ITR-U) was introduced to encourage voluntary tax compliance by allowing taxpayers to update their previously filed returns or file a return in certain eligible situations after the normal filing and revision period has ended.

It is particularly useful when a taxpayer discovers additional taxable income or identifies errors after the deadline for filing a revised return has expired.

An Updated Return cannot be filed in every situation. The Income-tax Act specifies conditions, restrictions, and additional tax implications that taxpayers must satisfy before filing ITR-U.

When Should You File an Updated Return?

You may consider filing an Updated Return if:

- You forgot to report certain taxable income.

- Additional financial information becomes available later.

- You discover an omission after the revised return deadline.

- You want to voluntarily correct your tax records.

However, an Updated Return cannot generally be used to reduce tax liability, claim additional refunds, or increase an already claimed refund. Taxpayers should carefully review the applicable legal provisions before filing.

Original Return vs Belated Return vs Revised Return vs Updated Return

Understanding the difference between these return types helps taxpayers choose the correct option.

| Return Type | Purpose | When Used |

|---|---|---|

| Original Return | First Income Tax Return filed for an Assessment Year | Before the applicable due date |

| Belated Return | Return filed after missing the original due date | After the due date, within the permitted time |

| Revised Return | Corrects mistakes in an already filed return | When errors or omissions are discovered within the revision period |

| Updated Return (ITR-U) | Updates income or corrects eligible omissions after the revision window | Subject to conditions specified under the Income-tax Act |

Choosing the correct type of return is essential to ensure compliance and avoid unnecessary issues during tax processing.

Step-by-Step Process to Correct an Already Filed Income Tax Return

If you identify an error after filing your Income Tax Return, follow these general steps:

Step 1: Identify the Mistake

Carefully review your filed return to determine the exact error.

Examples include:

- Missing income

- Incorrect deduction

- Wrong bank account details

- Incorrect TDS information

- Wrong ITR form

Step 2: Collect Supporting Documents

Before making corrections, gather all relevant documents such as:

- Form 16

- Form 26AS

- Annual Information Statement (AIS)

- Bank statements

- Interest certificates

- Investment proofs

- Capital gains statements

Having complete documentation helps ensure accurate reporting.

Step 3: Determine the Correct Return Type

Ask yourself:

- Is this my first return?

- Did I miss the due date?

- Am I correcting an already filed return?

- Has the revision period expired?

Your answers will help determine whether you need an Original Return, Belated Return, Revised Return, or Updated Return.

Step 4: Make the Necessary Corrections

Update the incorrect information carefully.

Examples include:

- Add omitted income.

- Correct tax calculations.

- Update bank account details.

- Modify deduction claims.

- Correct capital gains.

- Select the appropriate ITR form.

Double-check all entries before submission.

Step 5: Submit and Verify the Return

After making the corrections, submit the return through the Income Tax e-Filing portal and complete the required verification process.

A return is considered complete only after successful verification.

Common Mistakes Taxpayers Make

Many taxpayers unintentionally make mistakes while filing their Income Tax Returns.

Some of the most common errors include:

Ignoring AIS and Form 26AS

Always compare your Income Tax Return with the information available in your AIS and Form 26AS before filing.

Forgetting Interest Income

Many taxpayers report salary income correctly but forget to include:

- Savings account interest

- Fixed deposit interest

- Recurring deposit interest

These amounts are generally taxable unless specifically exempt.

Choosing the Wrong ITR Form

Selecting an incorrect ITR form may result in a defective return or processing delays.

Always determine your eligibility before choosing a form.

Claiming Incorrect Deductions

Taxpayers sometimes claim deductions without verifying eligibility.

Incorrect claims may attract scrutiny from the Income Tax Department.

Entering Incorrect Bank Details

Wrong bank account numbers or IFSC codes may delay tax refunds.

Verify your banking information carefully before submission.

Filing Without Verification

Submitting the return alone is not sufficient. The return must also be verified using one of the approved verification methods.

Failure to verify may result in the return being treated as invalid.

Tips to Avoid Filing Errors

Following a few simple practices can significantly reduce mistakes.

- Keep all financial documents ready before filing.

- Review AIS and Form 26AS.

- Verify TDS details.

- Check bank account information.

- Report all income sources.

- Choose the correct ITR form.

- Review deductions carefully.

- Verify your return immediately after filing.

- Keep copies of acknowledgement receipts for future reference.

Taking a little extra time before submission can save significant effort later.

Frequently Asked Questions

Can I file two original Income Tax Returns for the same Assessment Year?

No. Only one original Income Tax Return can be filed for a particular Assessment Year. If corrections are required, you should file the appropriate return permitted under the Income-tax Act.

What should I do if I forgot to report some income?

If you discover omitted income after filing your return, you should evaluate whether you are eligible to file a Revised Return or an Updated Return, depending on your circumstances and the applicable legal provisions.

Can I revise my Income Tax Return multiple times?

A revised return may be filed more than once if corrections are still required and the applicable legal conditions and time limits are satisfied. Each revised return replaces the previously filed return.

Will I receive a penalty if I correct my mistake?

Correcting genuine mistakes voluntarily is generally better than leaving errors unreported. However, depending on the nature of the correction and the applicable provisions, interest or additional tax may still apply.

Can I change my bank account after filing?

If the incorrect bank account details affect your Income Tax Return, you should update them using the appropriate procedure available on the Income Tax e-Filing portal or while filing an eligible corrected return.

Conclusion

Filing your Income Tax Return accurately is one of the most important aspects of tax compliance. Although you cannot file two original Income Tax Returns for the same Assessment Year, the Income-tax Act provides mechanisms to correct genuine mistakes through Revised Returns and Updated Returns (ITR-U), subject to the applicable rules and conditions.

Whether you forgot to report income, claimed an incorrect deduction, selected the wrong ITR form, or entered inaccurate information, it is always advisable to correct the mistake as soon as possible. Delaying corrections may lead to notices, additional tax liability, or other compliance issues.

Before filing any return, carefully review your financial records, compare them with your AIS and Form 26AS, verify all personal and banking details, and ensure you have selected the correct ITR form. A few extra minutes spent reviewing your return can help prevent costly mistakes and make the entire tax filing process smoother and stress-free.

If your situation is complex or you are unsure which type of return to file, seeking professional tax assistance can help ensure that your Income Tax Return is accurate, compliant, and filed correctly.