UPI has completely changed how Indians send and receive money.

From tea stalls to freelancers, almost everyone now uses apps like Google Pay, PhonePe, Paytm, and BHIM for daily transactions.

But recently, many people have started worrying about one thing:

“Can I get an income tax notice because of high UPI transactions?”

The short answer is — yes, in some cases.

However, not every large UPI transaction is suspicious. The Income Tax Department mainly looks for transactions that do not match your income profile or tax filings.

This guide explains when UPI transactions may attract scrutiny, what limits people should know, and how to stay safe legally.

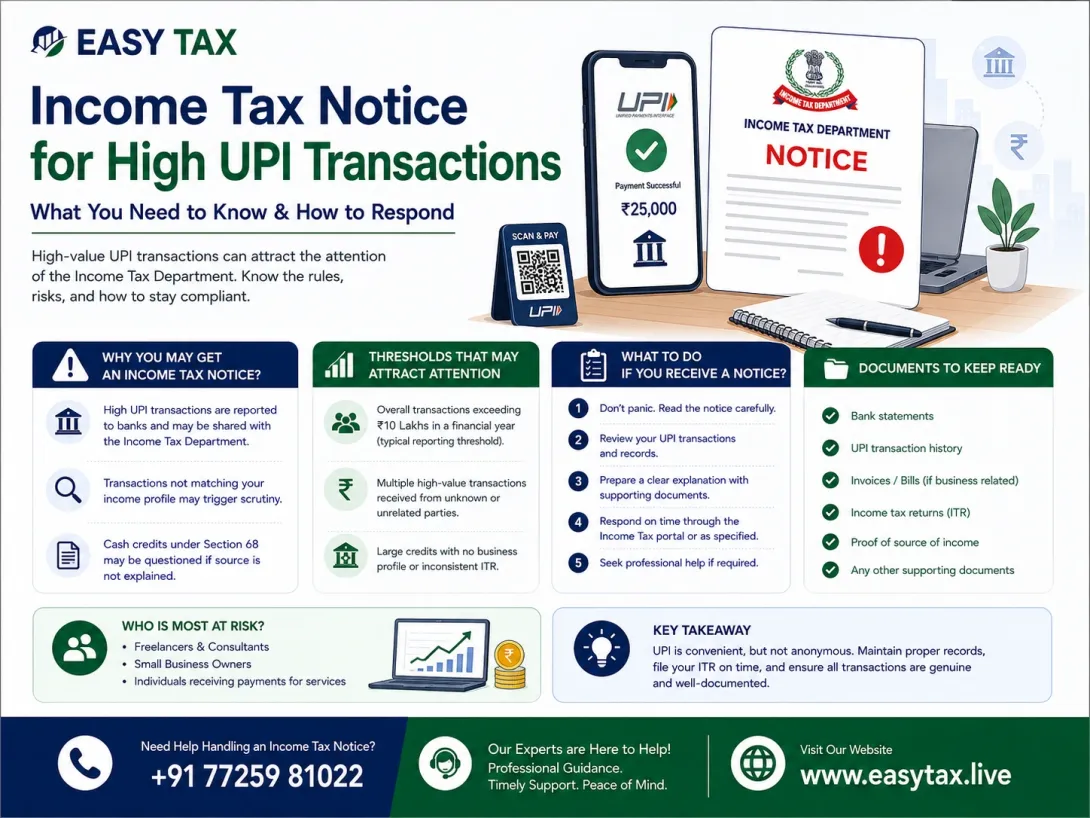

Are UPI Transactions Monitored by the Income Tax Department?

Yes. Financial transactions in India are increasingly tracked through digital systems.

Banks and payment platforms maintain records of:

- Money received

- Transaction frequency

- Linked PAN details

- Bank account activity

The Income Tax Department may review this information if:

- Your transactions look unusually high

- Your declared income is too low

- There are repeated business-like payments

- Your ITR does not match your financial activity

This does not mean every UPI payment is checked manually.

Most scrutiny happens through automated systems and data matching.

What Kind of UPI Transactions Can Trigger an Income Tax Notice?

Usually, normal personal transactions are not a problem.

Issues may arise when there are:

- Very high incoming payments

- Frequent business transactions on personal accounts

- Large unexplained credits

- Cash deposits linked with heavy UPI activity

- Mismatch between income and spending patterns

Example

A person files an ITR showing annual income of ₹3 lakh.

But their bank account receives:

- ₹25 lakh through UPI

- Hundreds of customer payments monthly

This mismatch may trigger scrutiny.

The department may ask:

- What is the source of income?

- Was business income disclosed?

- Was GST applicable?

- Were taxes properly paid?

Is There Any “Safe Limit” for UPI Transactions?

There is no officially declared “safe limit” for UPI transactions.

However, scrutiny risk generally increases when:

- Transactions become unusually high

- Activity resembles business operations

- Income declared in ITR is very low compared to credits

The key factor is:

Whether your transactions match your reported income.

A salaried employee receiving occasional family transfers usually has no issue.

But repeated commercial receipts without tax reporting can create problems.

Do Freelancers and Small Businesses Face Higher Risk?

Yes.

Freelancers, online sellers, consultants, traders, and creators often receive payments directly through UPI.

Many people:

- Use personal savings accounts

- Skip GST registration

- Do not report full income

- Ignore bookkeeping

This is where problems begin.

Common Examples

- Instagram sellers receiving daily UPI payments

- Freelancers accepting client payments through Google Pay

- Tuition teachers collecting fees digitally

- Small shops avoiding invoices

If the department notices regular commercial activity without proper reporting, a notice may be issued.

Can Family Transfers Through UPI Be Taxable?

Usually, no.

Money received from:

- Parents

- Spouse

- Siblings

- Close relatives

is generally not taxable under income tax rules.

However, problems can happen if:

- Transactions are extremely large

- No proper explanation exists

- Multiple accounts are used suspiciously

Keeping basic records is always a good idea for large transfers.

Can Personal UPI Accounts Be Used for Business?

Technically yes, but it is not recommended for growing businesses.

Using a personal account for business payments creates:

- Accounting confusion

- Tax reporting issues

- Difficulty during notices

- GST complications

A separate current account helps:

- Maintain clean records

- Track business income properly

- Build compliance credibility

What Happens If You Receive an Income Tax Notice?

Do not panic.

Many notices are simply requests for clarification.

The department may ask:

- Source of funds

- Nature of transactions

- Bank statements

- GST details

- Proof of income

Ignoring notices is a major mistake.

Responding properly and on time is important.

Common Mistakes That Trigger UPI-Related Tax Problems

1. Not Filing ITR

Some people assume small online income is invisible.

It is not.

2. Hiding Business Income

Frequent customer payments can indicate commercial activity.

3. Using Multiple Accounts

Splitting payments across accounts may still be traceable.

4. No Books or Records

Without invoices or records, explaining transactions becomes difficult.

5. Ignoring GST Rules

Some businesses receiving UPI payments may also require GST registration.

How to Stay Safe Legally

You do not need to fear digital payments.

You simply need proper compliance.

Good Practices Include:

- File ITR regularly

- Report all business income honestly

- Keep invoices and payment records

- Use separate business accounts

- Maintain GST compliance if applicable

- Avoid unexplained cash transactions

Transparency reduces notice risk significantly.

Real-Life Example

Neha is a freelance graphic designer in Pune.

She receives:

- ₹60,000 to ₹1 lakh monthly through UPI

- Payments from Indian startups and clients

Initially, she used her personal savings account and never filed GST.

Later, she received a compliance email asking for clarification on transactions.

After consulting a tax professional:

- She filed pending ITRs

- Registered properly

- Organized invoices

- Responded correctly

The issue was resolved without major penalties.

Final Thoughts

UPI itself is not the problem.

The real issue begins when:

- Income is hidden

- Transactions do not match tax returns

- Business activity is ignored

As digital payments grow in India, financial transparency is also increasing.

If your UPI activity is genuine and properly reported, there is usually nothing to worry about.

But if you receive large or frequent payments, especially for business or freelancing, it is smart to maintain proper tax compliance from the beginning.

That can save you from:

- Stress

- Notices

- Penalties

- Future legal complications

FAQs

Can UPI transactions trigger income tax notices?

Yes. High-value or suspicious transactions that do not match your declared income may attract scrutiny.

Is personal UPI monitored?

Banks and financial systems maintain transaction records that may be reviewed by tax authorities.

How much UPI transaction is safe?

There is no fixed limit. The key factor is whether transactions match your income profile and tax filings.

Do freelancers get tax notices for UPI payments?

They can, especially if business income is not properly disclosed.

Are family transfers taxable?

Usually no, if received from specified relatives under income tax rules.

Need Help With an Income Tax Notice?

Received a notice for bank or UPI transactions?

Get expert support from EasyTax.live before replying to the department. Professional guidance can help you avoid unnecessary penalties and respond correctly with proper documentation.