National Pension System (NPS): Benefits, Tax Savings & Complete Investment Guide (2026)

Planning for retirement is one of the most important financial decisions in life. A strong pension plan ensures that you remain financially independent even after you stop working. Among the available retirement options in India, the National Pension System (NPS) is one of the most reliable, flexible, and tax-efficient investment tools.

Regulated by the Pension Fund Regulatory and Development Authority (PFRDA), NPS is a government-backed retirement scheme designed to help individuals build a long-term pension corpus through systematic investments.

In this detailed guide, we will explain what NPS is, its benefits, tax advantages, withdrawal rules, and how it helps in building a secure financial future.

What is the National Pension System (NPS)?

The National Pension System (NPS) is a voluntary, long-term retirement savings scheme launched by the Government of India. It encourages individuals to invest regularly during their working life so they can receive a stable income after retirement.

NPS is open to:

- Indian citizens (resident or non-resident)

- Employees (government and private sector)

- Self-employed individuals

It allows investment in a mix of:

- Equity (stocks)

- Corporate bonds

- Government securities

This combination helps balance risk and return, making it a suitable retirement planning option.

Key Objective of NPS

The main goal of NPS is simple:

👉 To create a disciplined retirement corpus that provides financial stability after retirement.

It ensures that individuals do not depend entirely on savings or family support in old age.

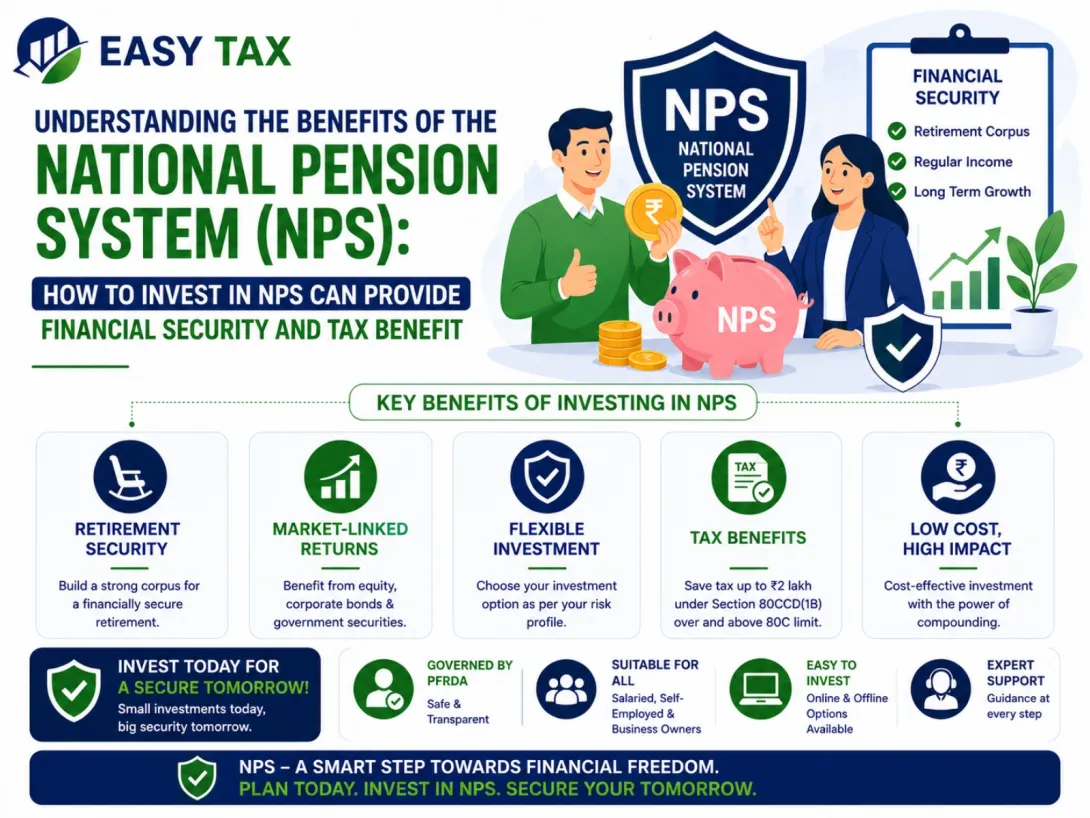

Major Benefits of National Pension System (NPS)

1. Long-Term Retirement Security

The biggest advantage of NPS is financial security after retirement. Regular contributions during working years build a strong pension fund.

At retirement:

- Up to 60% of the corpus can be withdrawn as a lump sum

- The remaining 40% is used to purchase an annuity

- This provides monthly pension income

This ensures a steady post-retirement cash flow.

2. Excellent Tax Benefits

NPS is one of the most tax-efficient investment options in India.

Under Section 80CCD(1):

- Salaried individuals can claim up to 10% of salary (Basic + DA)

- Self-employed individuals can claim up to 20% of gross income

- This falls under the ₹1.5 lakh limit of Section 80C

Under Section 80CCD(1B):

- Additional deduction of ₹50,000

- This is over and above Section 80C limit

Under Section 80CCD(2):

- Employer contribution up to 10% of salary is fully tax-free

- This is a major benefit for salaried employees

✔ NPS = One of the highest tax-saving instruments in India

3. Flexible Investment Options

NPS allows investors to choose how their money is invested.

Active Choice:

You decide allocation between:

- Equity (E)

- Corporate bonds (C)

- Government securities (G)

Auto Choice:

The system automatically adjusts allocation based on age:

- Higher equity exposure when young

- Lower risk as retirement approaches

This ensures balanced risk management over time.

4. Low Cost, High Returns

NPS is known for having one of the lowest fund management charges in India.

Lower charges mean:

✔ Higher long-term returns

✔ Better retirement corpus growth

✔ Efficient wealth accumulationOver long periods, this makes a huge difference.

5. Portability Across Jobs

NPS is fully portable.

You can:

- Change jobs

- Move cities

- Switch sectors

Your NPS account remains the same throughout your working life.

This makes it ideal for:

- Private employees

- Government employees

- Freelancers

6. Partial Withdrawal Flexibility

NPS allows partial withdrawal under specific conditions after 3 years.

You can withdraw up to:

- 25% of your contributions

Allowed purposes include:

- Higher education

- Marriage expenses

- Medical emergencies

- Home purchase

This provides financial flexibility during emergencies.

7. Tax-Free Lump Sum at Retirement

At retirement:

- 60% of corpus = tax-free withdrawal

- 40% = must be used for annuity purchase

This structure ensures:

✔ Immediate financial support

✔ Long-term pension security8. Regulated & Safe Investment

NPS is regulated by PFRDA, ensuring:

- Transparency

- Security

- Accountability

- Investor protection

It is a government-backed scheme, making it highly trustworthy.

Who Can Invest in NPS?

Any individual aged:

- 18 to 70 years

Eligible investors:

- Salaried employees

- Self-employed professionals

- NRIs (Non-Resident Indians)

How to Open an NPS Account?

Opening an NPS account is simple:

Online Method:

- Visit eNPS portal

- Register using Aadhaar or PAN

- Complete KYC verification

- Choose investment option

- Make initial contribution

Offline Method:

Through authorized Point of Presence (POP):

- Banks

- Financial institutions

- Registered financial advisors

NPS vs Other Retirement Options

Feature NPS PPF Fixed Deposit Returns Market-linked (higher potential) Fixed Fixed Tax Benefit Very High High Low Flexibility High Low Medium Risk Moderate Low Low ✔ NPS offers better long-term wealth creation potential

Common Mistakes to Avoid in NPS

- Not starting early

- Choosing wrong asset allocation

- Ignoring tax benefits

- Not reviewing fund performance

- Withdrawing unnecessarily

Why NPS is Important for Retirement Planning

NPS ensures:

- Financial independence after retirement

- Stable monthly pension income

- Long-term wealth creation

- Tax-efficient savings

In simple terms:

👉 It builds discipline + savings + security togetherWhy Choose Easy Tax Jaipur for NPS Guidance?

Easy Tax Jaipur helps individuals and businesses with:

- NPS account setup

- Investment planning

- Tax benefit optimization

- Retirement strategy guidance

- Financial advisory services

With expert support, investors can:

✔ Maximize tax savings

✔ Choose better fund allocation

✔ Plan retirement effectivelyFrequently Asked Questions (FAQs)

1. Is NPS a safe investment?

Yes, it is regulated by PFRDA and backed by the government.

2. Can I withdraw money before retirement?

Partial withdrawal is allowed after 3 years under specific conditions.

3. Is NPS better than PPF?

NPS offers higher returns but comes with market-linked risk.

4. Can NRIs invest in NPS?

Yes, NRIs are eligible to open an NPS account.

5. What is the minimum contribution?

Minimum contribution is low and affordable for all income groups.

Conclusion

The National Pension System (NPS) is one of the most powerful retirement planning tools in India. It offers a perfect combination of tax savings, long-term wealth creation, and financial security.

With flexible investment options, low management costs, and government backing, NPS is ideal for anyone planning a secure retirement.

If used wisely, it can help you build a strong financial foundation for your future.

For expert guidance on NPS planning and tax benefits, consulting