Many salaried employees in India are confused about one major question:

“Is the new tax regime actually better for saving tax?”

Since the government introduced the new tax regime, taxpayers now have two choices:

- Old Tax Regime

- New Tax Regime

The new regime offers lower tax rates, but many common deductions and exemptions are removed.

Still, that does not mean tax saving becomes impossible.

In fact, many salaried employees can legally reduce their tax burden even under the new regime if they plan properly.

This guide explains the best tax saving options available under the new tax regime in 2026 in simple language.

What Is the New Tax Regime?

The new tax regime is an alternative income tax system introduced to simplify taxation for individuals.

It provides:

- Lower income tax slab rates

- Less paperwork

- Fewer deductions and exemptions

However, taxpayers usually give up deductions like:

- 80C investments

- HRA exemption

- Home loan benefits (self-occupied property)

- Medical insurance deductions under 80D

Despite this, several tax-saving opportunities still exist.

New Tax Regime Slabs for FY 2025-26

| Income Range | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

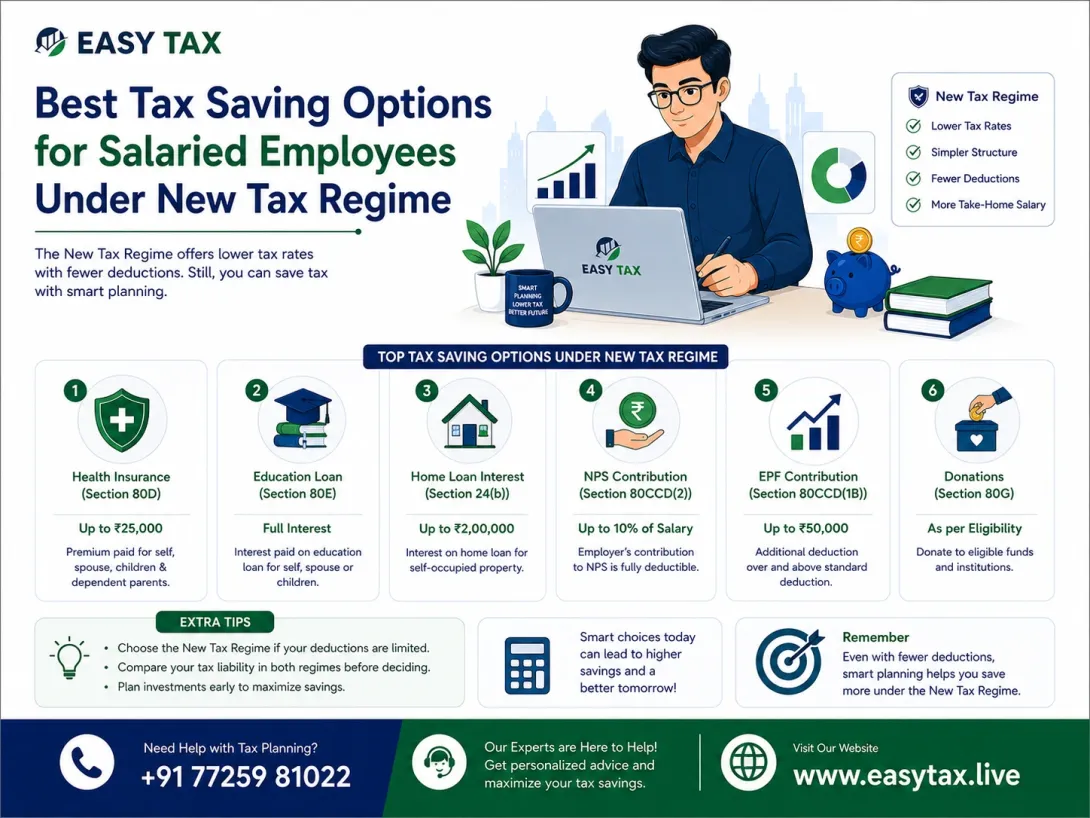

1. Standard Deduction Still Available

One of the biggest reliefs for salaried employees is that the standard deduction is allowed even under the new tax regime.

Eligible employees can claim:

- ₹75,000 standard deduction

This directly reduces taxable salary income without requiring any investment proof.

2. Employer Contribution to NPS

This is one of the best tax-saving tools still available.

Employer contribution to the National Pension System (NPS) under Section 80CCD(2) remains deductible under the new regime.

Benefits include:

- Extra tax savings

- Retirement planning

- Lower taxable income

Many employees ignore this option even though it can save significant tax annually.

3. EPF Contributions Continue Automatically

Employee Provident Fund (EPF) deductions from salary continue as usual.

While separate 80C benefits may not apply under the new regime, EPF still helps:

- Create long-term savings

- Build retirement security

- Maintain disciplined investing

4. Tax-Free Allowances From Employers

Some allowances may still provide benefits depending on salary structure and company policies.

Examples include:

- Travel reimbursements

- Telephone reimbursement

- Food coupons

- Internet reimbursement

Smart salary restructuring can legally reduce taxable income.

5. Leave Encashment Benefits

Leave encashment received during retirement may enjoy tax exemptions under applicable rules.

Employees should understand these benefits before retirement planning.

6. Gratuity Exemption

Gratuity received from employers can also be partially or fully tax-exempt based on conditions.

This becomes important for long-term salaried employees nearing retirement.

7. Family Pension Deduction

Family pension recipients can still claim limited deductions under the new regime.

This provides relief for dependent family members receiving pension income.

Should You Choose Old or New Tax Regime?

There is no single answer for everyone.

The better option depends on:

- Your salary structure

- Home loan status

- Investment habits

- Insurance premiums

- Total deductions available

Generally:

- The new regime suits people with fewer deductions.

- The old regime may benefit heavy investors and home loan holders.

Example Comparison

Rahul earns ₹14 lakh annually.

He does not have:

- Home loan

- Large 80C investments

- Major deductions

In his case, the new tax regime may result in lower tax liability.

On the other hand, Priya invests heavily in:

- PPF

- ELSS

- Life insurance

- Home loan repayment

She may save more under the old regime.

Common Mistakes Salaried Employees Make

1. Choosing Without Calculation

Many people randomly select the new regime without comparing both options.

2. Ignoring Employer NPS

This is one of the biggest missed tax-saving opportunities.

3. Not Reviewing Salary Structure

Proper salary restructuring can improve tax efficiency.

4. Filing Incorrect ITR

Choosing the wrong regime during filing may create complications later.

How to Reduce Tax Legally Under the New Regime

- Claim standard deduction

- Use employer NPS contribution

- Optimize salary structure

- Maintain proper tax planning

- Review tax calculations yearly

Even small planning decisions can save thousands of rupees every year.

Final Thoughts

The new tax regime is not completely “tax-free,” but it can simplify taxation for many salaried employees.

The key is understanding:

- Which deductions are still available

- How your salary is structured

- Whether old or new regime suits your income pattern

Before filing your ITR, always compare both regimes carefully instead of blindly selecting one.

Proper tax planning can help you:

- Reduce tax liability

- Increase savings

- Avoid filing mistakes

- Improve financial planning

FAQs

Is standard deduction available in the new tax regime?

Yes, salaried employees can claim standard deduction under the new regime.

Can I claim 80C deductions in the new tax regime?

Most 80C deductions are not available under the new regime.

Is NPS beneficial under the new tax regime?

Yes, employer contribution to NPS remains tax deductible.

Which regime is better for salaried employees?

It depends on your deductions, investments, and salary structure.

Can I switch between old and new tax regimes?

Salaried employees can generally switch every financial year while filing ITR.

Need Help Choosing the Right Tax Regime?

Confused between the old and new tax regime?

Get expert tax planning and ITR filing support from EasyTax.live. Our professionals help salaried employees legally reduce taxes and avoid filing mistakes.