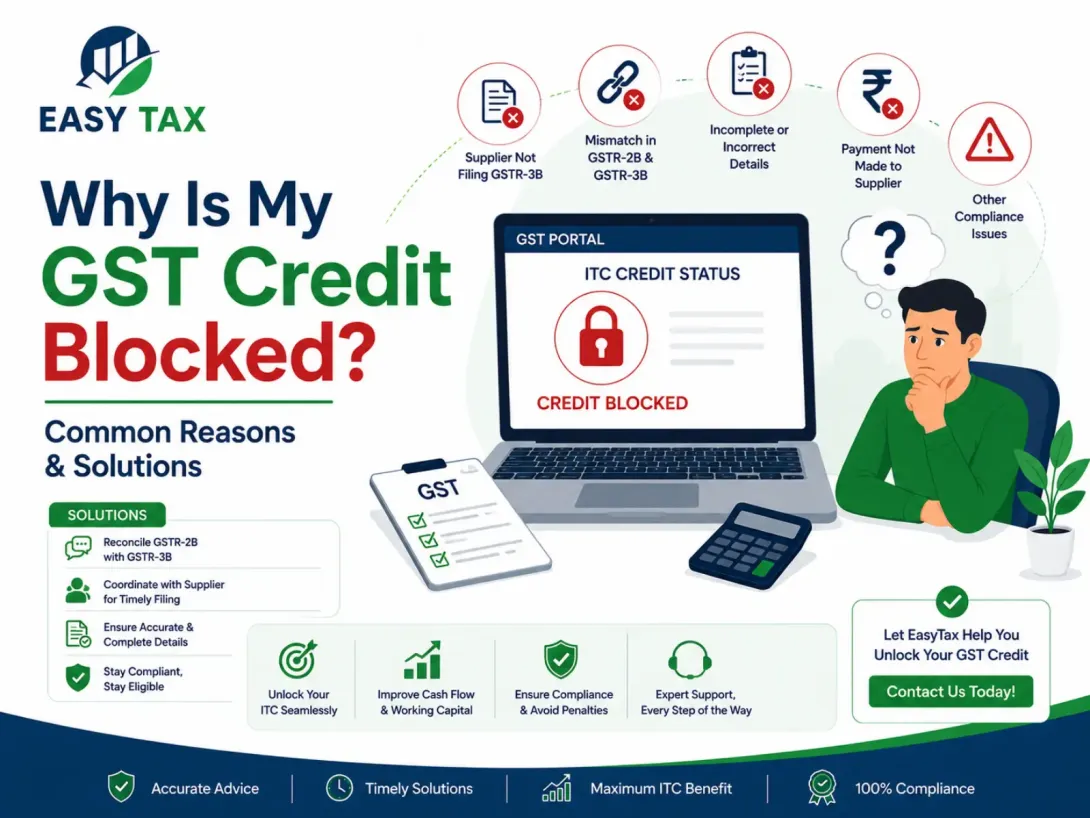

If you are wondering why your electronic credit ledger is blocked, you are not alone. Many business owners discover the issue only when they try to utilize Input Tax Credit (ITC) while filing GST returns and find that the credit is unavailable.

A blocked GST credit can impact your cash flow, increase tax payments, and disrupt business operations. For small businesses and growing companies, even temporary restrictions can create financial pressure.

The GST department generally blocks ITC when it believes that the credit may have been claimed incorrectly or that further verification is required. Most such actions are taken under Rule 86A of the CGST Rules.

This guide explains why GST credit gets blocked, how Rule 86A works, when officers can restrict ITC usage, and what steps you can take to resolve the issue.

What does a blocked GST credit mean?

A blocked GST credit means you cannot use some or all of the Input Tax Credit available in your Electronic Credit Ledger to pay GST liability.

When credit is blocked, the amount may still appear in your ledger, but you cannot utilize it for GST payments until the restriction is removed.

Input Tax Credit (ITC) is the credit you receive for GST paid on business purchases. This credit reduces the GST you must pay on sales.

A blocked credit situation may affect:

- GST return filing

- Working capital

- Tax planning

- Vendor payments

- Compliance management

For example: A manufacturing company in Jaipur with ₹5 lakh of ITC may suddenly find that the credit cannot be utilized despite appearing in the Electronic Credit Ledger.

This restriction usually requires investigation and corrective action before the credit becomes available again.

Why is my electronic credit ledger blocked?

Your Electronic Credit Ledger may be blocked if GST authorities believe that the Input Tax Credit has been claimed fraudulently or requires verification.

The GST department uses Rule 86A to protect revenue when officers have reasons to believe that the credit may not be genuine. The restriction is preventive in nature and is often applied while an investigation is ongoing.

Common reasons include:

Supplier-Related Issues

- Supplier failed to file GST returns

- Supplier disappeared after issuing invoices

- Supplier registration was cancelled

- Supplier involved in suspicious transactions

Invoice-Related Issues

- Fake invoices

- Duplicate invoices

- Incorrect GSTIN details

- Mismatched invoice information

Business Compliance Issues

- Improper record maintenance

- Unexplained transactions

- Non-availability of supporting documents

- Suspicious claim patterns

For example: If a trader in Delhi claims ITC based on invoices issued by a supplier later found to be non-existent, authorities may temporarily block the credit.

Not every blocked credit case involves fraud. Sometimes documentation gaps trigger compliance reviews.

What is Rule 86A under GST?

Rule 86A allows GST officers to temporarily block the utilization of Input Tax Credit when they have reasons to believe that the credit has been fraudulently claimed.

Rule 86A of the CGST Rules was introduced to prevent misuse of ITC through fake invoices and fraudulent transactions. It empowers authorized officers to restrict the use of credit during investigations.

The rule may be invoked when:

- Credit is claimed using fake invoices

- Goods or services were never received

- Suppliers do not exist

- Tax was not actually paid to the government

- Documents supporting the claim are unreliable

Key Features of Rule 86A

| Feature | Details | Impact |

|---|---|---|

| Temporary Restriction | Credit cannot be used | Cash flow affected |

| Investigation Based | Triggered by suspicion | Verification required |

| Officer Approval | Authorized officer required | Legal oversight |

| Time Bound | Cannot continue indefinitely | Protection for taxpayers |

For businesses, Rule 86A is one of the most important provisions governing GST credit utilization.

Can GST officers block ITC without notice?

GST officers may restrict ITC under Rule 86A without issuing a prior notice in certain circumstances, but the action must be supported by valid reasons.

Many taxpayers assume that a formal show-cause notice is mandatory before every restriction. However, Rule 86A allows officers to act when they believe immediate intervention is necessary to protect government revenue.

This generally happens when:

- Fraud indicators are detected

- High-risk transactions are identified

- Fake invoice networks are suspected

- Supplier investigations reveal irregularities

However, the officer's decision cannot be arbitrary. The restriction should be:

- Based on evidence

- Recorded in writing

- Supported by reasonable belief

- Subject to legal scrutiny

For example: If authorities uncover a network issuing fake invoices across multiple states, they may block related ITC before issuing detailed notices.

Businesses should immediately seek clarification and gather supporting documents if such restrictions occur.

What are the most common reasons GST credit gets blocked?

The most common reasons GST credit gets blocked include fake invoices, supplier defaults, document deficiencies, and suspected fraudulent claims.

Understanding the exact reason behind the restriction is essential because the solution often depends on the specific issue identified by authorities.

Top Reasons for GST Credit Blocking

| Reason | Description | Risk Level | Common Impact |

|---|---|---|---|

| Fake Invoices | Non-genuine invoices used | High | ITC Restriction |

| Supplier Default | Vendor non-compliance | High | Credit Suspension |

| Missing Documents | Insufficient proof | Medium | Verification Required |

| Mismatched Records | Invoice discrepancies | Medium | Compliance Review |

| Fraud Investigation | Ongoing inquiry | High | Ledger Restriction |

Common Red Flags

- High ITC claims compared to turnover

- Frequent transactions with unknown vendors

- Sudden spikes in purchases

- Missing transportation records

- Incorrect GST filings

For example: A wholesaler in Ahmedabad may purchase goods from a supplier who later stops filing GST returns. During departmental scrutiny, related ITC may become subject to restriction until verification is completed.

Businesses should regularly monitor supplier compliance to reduce such risks.

How can you identify the exact reason for blocked GST credit?

You can identify the exact reason by reviewing GST notices, departmental communications, supplier compliance records, and transaction documents.

Many businesses panic when they discover blocked credit. However, the first step should always be understanding the basis of the restriction before taking corrective action.

Investigation Checklist

- Check GST portal notifications

- Review notices received

- Verify supplier GST status

- Reconcile purchase invoices

- Review GSTR-2B entries

- Match transportation records

- Verify payment records

Important documents include:

- Tax invoices

- E-Way Bills

- Purchase orders

- Bank payment proofs

- Delivery challans

- Vendor agreements

For example: A business in Mumbai discovering blocked ITC should first verify whether the issue originates from a supplier compliance failure or an internal documentation problem.

Identifying the actual cause early can significantly speed up the resolution process.

How can you unblock your GST credit ledger?

You can unblock your GST credit ledger by identifying the reason for the restriction, gathering supporting documents, responding to GST notices, and demonstrating that the claimed Input Tax Credit is genuine.

A blocked Electronic Credit Ledger does not automatically mean that the credit is permanently lost. In many cases, businesses can restore access by providing proper documentation and cooperating with GST authorities.

The exact resolution process depends on why the credit was blocked.

Common Steps to Unblock GST Credit

- Identify the reason for restriction

- Review Rule 86A communications

- Verify supplier compliance

- Gather supporting documents

- Submit explanations and evidence

- Respond to GST notices

- Follow up with authorities

- Seek professional assistance if required

Businesses should avoid making assumptions and instead focus on evidence-based responses.

For example: A trader in Jaipur whose supplier later defaulted on GST filings may need to prove that goods were actually received and payments were genuinely made.

What is the Rule 86A GST unblocking procedure?

The Rule 86A GST unblocking procedure generally involves proving that the Input Tax Credit claim is legitimate and that the grounds for restriction no longer exist.

GST officers review supporting records before deciding whether blocked credit should be restored. The process may vary depending on the facts of each case.

Documents Commonly Requested

- Tax invoices

- E-Way Bills

- Delivery challans

- Purchase orders

- Payment proofs

- Bank statements

- Supplier agreements

- Goods receipt records

Typical Unblocking Process

| Step | Action | Purpose |

|---|---|---|

| Review | Officer examines case | Verify facts |

| Documentation | Business submits records | Support claim |

| Verification | Department cross-checks data | Confirm genuineness |

| Decision | Restriction reviewed | Restore or continue block |

For example: A manufacturer in Surat may submit transportation records, invoices, and payment proofs to establish that purchases were genuine.

Complete documentation often plays a critical role in resolving disputes.

How long can GST credit remain blocked?

GST credit cannot remain blocked indefinitely under Rule 86A.

The law provides safeguards to ensure that restrictions are temporary rather than permanent. As per Rule 86A, restrictions generally cease after one year from the date of imposition unless separate legal proceedings justify further action.

This time limitation protects taxpayers from indefinite restrictions.

Important Rule 86A Time Limit Facts

- Restriction is temporary

- One-year limitation generally applies

- Review should be evidence-based

- Credit may be restored earlier if issues are resolved

For example: If a restriction was imposed in June 2026, the Rule 86A block cannot ordinarily continue beyond the permitted period unless supported by other legal actions.

Businesses should track dates carefully and maintain records of all communications.

What should you do after receiving a blocked ITC notice?

You should review the notice carefully, identify the allegations, collect supporting evidence, and submit a clear response within the specified timeline.

Many businesses make the mistake of responding emotionally or without proper documentation. A professional, fact-based response is far more effective.

Response Checklist

- Read the notice thoroughly

- Identify disputed transactions

- Verify supplier information

- Collect invoices and records

- Prepare a written explanation

- Submit documents within deadlines

- Retain acknowledgment records

A structured response improves the chances of a favorable outcome.

For example: A wholesaler in Delhi receiving a notice related to supplier compliance issues should provide evidence of actual purchases, payments, and goods receipt.

What should a reply to a blocked ITC notice contain?

A reply should clearly explain the transaction, provide supporting evidence, and demonstrate that the Input Tax Credit claim complies with GST provisions.

The objective is to establish that the credit was claimed in good faith and supported by genuine business transactions.

Common Elements of a Reply

- Reference to notice number

- Business details

- Explanation of disputed transaction

- Supporting invoice details

- Payment evidence

- Goods receipt proof

- Legal justification

- Request for restoration of credit

Sample Structure

| Section | Purpose |

|---|---|

| Introduction | Identify taxpayer |

| Transaction Summary | Explain disputed credit |

| Supporting Evidence | Attach records |

| Legal Position | Reference GST provisions |

| Closing Request | Request restoration |

A well-documented reply often carries more weight than lengthy explanations without evidence.

What is a negative balance in the Electronic Credit Ledger?

A negative balance situation generally indicates an adjustment, system issue, reversal, or compliance-related discrepancy requiring immediate review.

The Electronic Credit Ledger records available GST credit. Businesses should regularly monitor the ledger to identify unusual entries and investigate discrepancies promptly.

Potential reasons include:

- ITC reversals

- System adjustments

- Compliance corrections

- Departmental actions

- Data mismatches

Immediate Actions

- Review GST returns

- Check reversal entries

- Verify notices received

- Reconcile purchase records

- Consult a GST expert if necessary

For example: A business noticing a sudden reduction in available ITC should reconcile GSTR-2B data with ledger entries before assuming an error exists.

Timely investigation prevents further compliance complications.

What practical examples explain blocked GST credit situations?

Real-world examples help businesses understand why restrictions occur and how they can be resolved. Many blocked credit cases arise from supplier-related issues rather than deliberate wrongdoing by the recipient business.

Example 1: Supplier Non-Compliance

A Jaipur electronics dealer purchases goods from a supplier who later stops filing GST returns. During departmental scrutiny, related ITC is temporarily restricted until transaction authenticity is verified.

Example 2: Missing Documentation

A Delhi trading company claims ITC but cannot produce transportation records during review. Authorities seek additional evidence before allowing credit utilization.

Example 3: Fake Invoice Investigation

A network of businesses is investigated for issuing fake invoices. Even genuine recipients may experience temporary restrictions until transactions are verified.

These examples highlight the importance of maintaining complete records.

How can businesses reduce the risk of blocked GST credit?

Businesses can reduce risk by strengthening compliance systems, verifying suppliers, and maintaining accurate documentation.

Preventive compliance is often easier and less expensive than resolving blocked credit disputes later.

Best Practices for Businesses

- Verify supplier GST registration regularly

- Monitor supplier return filing status

- Match invoices with GSTR-2B

- Maintain transportation records

- Preserve payment proofs

- Conduct vendor due diligence

- Reconcile GST records monthly

- Respond quickly to notices

Compliance Comparison Table

| Practice | Purpose | Benefit | Risk Reduction |

|---|---|---|---|

| Supplier Verification | Confirm legitimacy | Stronger compliance | High |

| Monthly Reconciliation | Detect mismatches | Early correction | High |

| Documentation Storage | Support claims | Audit readiness | High |

| Notice Monitoring | Faster response | Better outcomes | Medium |

A proactive compliance strategy significantly reduces the likelihood of ITC restrictions.

What is blocked credit under Section 17(5) of the GST Act?

Blocked credit under Section 17(5) refers to specific purchases and expenses for which Input Tax Credit (ITC) cannot be claimed, even if GST has been paid.

Section 17(5) of the CGST Act contains a list of goods and services where ITC is specifically restricted. These restrictions apply regardless of whether the purchase is used for business purposes.

Many taxpayers confuse blocked credit under Section 17(5) with credit blocked under Rule 86A. However, these are completely different concepts.

Key Difference

| Rule 86A Block | Section 17(5) Block |

|---|---|

| Temporary restriction | Permanent restriction |

| Investigation-based | Law-based restriction |

| Credit may be restored | Credit generally unavailable |

| Compliance issue | Eligibility issue |

Understanding this distinction helps businesses avoid claiming ineligible credits.

What are the most common blocked credits under GST in 2026?

The most common blocked credits relate to motor vehicles, employee benefits, personal consumption, gifts, and certain construction-related expenses.

Many businesses unknowingly claim ineligible credits and later face notices or reversals during GST scrutiny.

Common Blocked ITC List for Businesses (2026)

| Expense Type | ITC Allowed? | Notes |

|---|---|---|

| Personal Expenses | No | Not business-related |

| Employee Gifts | Usually No | Subject to conditions |

| Club Membership | No | Restricted |

| Health Club Services | No | Restricted |

| Personal Travel Benefits | No | Employee benefit |

| Motor Cars | Generally No | Exceptions apply |

| Food & Beverages | Generally No | Exceptions apply |

| Construction Services | Usually No | Subject to conditions |

| Works Contract Services | Usually No | Certain restrictions |

| Lost or Destroyed Goods | No | Ineligible |

Businesses should review Section 17(5) carefully before claiming ITC.

Can you claim GST input tax credit on car purchases?

In most cases, GST input tax credit on motor cars is not available.

The GST law generally blocks ITC on motor vehicles used for passenger transportation with seating capacity up to thirteen persons, including the driver.

Exceptions Where ITC May Be Available

- Vehicle resale businesses

- Driving schools

- Passenger transportation services

- Vehicle leasing businesses

For example: A Jaipur-based automobile dealership purchasing cars for resale may be eligible to claim ITC. However, a consulting company purchasing a director's vehicle generally cannot claim the credit.

Can you claim GST ITC on office renovation and construction?

In most situations, GST paid on construction and certain renovation activities is blocked under GST provisions.

Construction-related credits are among the most misunderstood areas of GST compliance.

Typically Restricted

- Office building construction

- Structural improvements

- Immovable property creation

- Major renovation projects

May Require Detailed Review

- Repairs

- Maintenance

- Temporary installations

- Certain movable assets

For example: Constructing a new office building in Ahmedabad generally does not qualify for ITC.

The exact treatment depends on the nature of the expense.

Is GST on corporate health insurance blocked?

GST on corporate health insurance may be blocked unless specific business-related exceptions apply.

Many employers provide health insurance to employees as part of compensation packages. The ITC treatment depends on:

- Legal requirements

- Nature of employment

- Applicable GST provisions

- Specific business circumstances

Businesses should review current GST rules before claiming such credits. Improper claims may lead to reversals and notices.

Can businesses claim ITC on staff food and catering expenses?

GST on food and catering services is generally blocked unless specific exceptions are available.

Food and catering expenses are frequently questioned during GST audits.

Commonly Restricted

- Employee meals

- Staff refreshments

- Corporate dining expenses

- General food services

Potential Exceptions

- Statutory obligations

- Certain employer requirements

- Industry-specific situations

For example: If a law requires a factory to provide canteen facilities, the ITC treatment may differ from ordinary employee meal expenses.

Businesses should examine eligibility carefully before claiming credit.

Is GST credit available on gifts provided to employees?

GST credit on gifts provided to employees is generally not available under Section 17(5).

Many businesses distribute gifts during festivals, annual events, and employee recognition programs. Examples include:

- Gift hampers

- Electronics

- Vouchers

- Promotional gifts

Such credits are often restricted under GST provisions. Businesses should maintain separate records for employee benefit expenses to avoid compliance issues.

Can businesses claim ITC on hotel stays?

GST credit on hotel accommodation may be available or restricted depending on the business purpose and circumstances.

Hotel-related ITC often creates confusion because eligibility depends heavily on how the service is used. Factors considered include:

- Business purpose

- Nature of travel

- Documentation

- GST registration details

For example: Accommodation booked for legitimate business travel may be treated differently from personal travel expenses.

Proper invoices and supporting records are essential.

Frequently Asked Questions

Why is my electronic credit ledger blocked under GST?

Can GST officers block ITC without issuing a notice?

How long can GST credit remain blocked under Rule 86A?

What documents help unblock GST credit?

What is the Rule 86A GST unblocking procedure?

Can supplier non-compliance block my GST credit?

What is the difference between Rule 86A and Section 17(5)?

Is blocked GST credit permanently lost?

How can businesses avoid blocked GST credit issues?

Conclusion

A blocked GST credit can create serious cash flow and compliance challenges, but it does not always mean the credit is permanently unavailable. In many cases, the issue can be resolved through proper documentation, supplier verification, and timely responses to GST authorities.

The most important step is understanding why the restriction was imposed. Whether the issue relates to Rule 86A, supplier non-compliance, invoice mismatches, or documentation deficiencies, identifying the root cause is essential for resolution.

If your business is facing GST credit restrictions, Rule 86A notices, ITC disputes, or electronic credit ledger issues, EasyTax can help you review the case, prepare responses, verify compliance records, and guide you through the GST credit restoration process.