Understanding Income Tax Slabs: How to Lower Your Tax Bill Legally in 2026

Paying taxes is a legal responsibility, but paying more tax than necessary is not. Many individuals and business owners end up paying higher taxes simply because they do not fully understand how income tax slabs work or how to take advantage of available tax-saving opportunities.

In India, income tax is calculated based on tax slabs, which determine the rate of tax applicable to different levels of income. Understanding these slabs is essential for effective tax planning, maximizing deductions, and reducing your overall tax liability legally.

Whether you are a salaried employee, freelancer, consultant, investor, startup founder, or business owner, learning how tax slabs work can help you make smarter financial decisions and improve your long-term financial health.

In this complete guide, we explain income tax slabs, how taxes are calculated, tax-saving strategies, and practical ways to lower your tax bill in 2026.

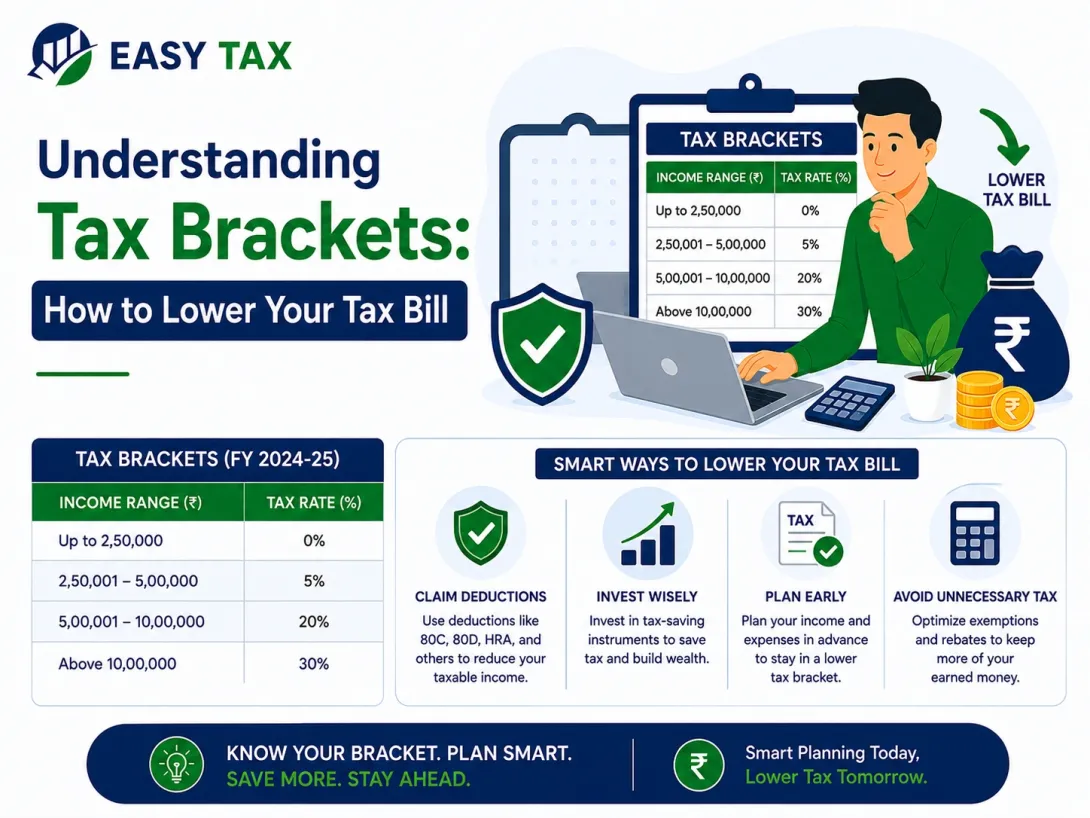

What Are Income Tax Slabs?

Income tax slabs are income ranges that determine how much tax a person must pay.

India follows a progressive taxation system, which means higher income levels are taxed at higher rates.

Instead of applying a single tax rate to your entire income, different portions of your income are taxed at different rates according to the applicable tax slabs.

This system ensures fairness by requiring higher earners to contribute more while providing relief to lower-income taxpayers.

Why Understanding Tax Slabs Is Important

Many taxpayers assume that moving into a higher tax slab means their entire income will be taxed at the higher rate.

This is a common misconception.

Only the income exceeding a specific slab limit is taxed at the higher rate.

Understanding this concept helps taxpayers:

- Plan finances effectively

- Avoid tax misconceptions

- Make informed investment decisions

- Reduce tax liability legally

- Optimize tax-saving opportunities

Income Tax Regimes in India

Taxpayers currently have the option to choose between:

New Tax Regime

The new tax regime offers:

- Lower tax rates

- Simplified structure

- Fewer deductions and exemptions

It is often preferred by individuals who do not claim significant deductions.

Old Tax Regime

The old tax regime allows:

- Various deductions

- Tax exemptions

- Investment-linked tax benefits

It is often beneficial for taxpayers who actively invest in tax-saving instruments.

Choosing the right regime is an important part of tax planning.

How Income Tax Slabs Work

Suppose your taxable income falls into multiple tax slabs.

Different portions of your income are taxed at different rates.

This means:

- Lower income portions are taxed at lower rates

- Higher income portions are taxed at higher rates

Understanding this structure helps taxpayers estimate their actual tax burden more accurately.

Common Sources of Taxable Income

Income can arise from various sources, including:

Salary Income

- Basic salary

- Bonuses

- Allowances

- Incentives

Business Income

- Professional income

- Freelance earnings

- Business profits

Capital Gains

- Stock market gains

- Mutual fund profits

- Property sales

Rental Income

- Residential property rent

- Commercial property income

Interest Income

- Fixed deposits

- Savings accounts

- Bonds

All taxable income sources should be reported accurately.

Smart Ways to Lower Your Tax Bill Legally

1. Claim Eligible Tax Deductions

Many taxpayers miss deductions that could significantly reduce taxable income.

Common deductions include:

Section 80C

Eligible investments such as:

- PPF

- ELSS

- EPF

- Life Insurance Premiums

- Tax-Saving Fixed Deposits

Section 80D

Health insurance premiums for:

- Self

- Spouse

- Children

- Parents

Section 80CCD

Contributions to pension schemes.

Proper use of deductions can lower taxable income substantially.

2. Optimize Salary Structure

Salaried employees can reduce taxes through proper salary planning.

Tax-efficient components may include:

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Employer retirement contributions

- Reimbursements

A well-structured salary package improves tax efficiency.

3. Invest for Long-Term Wealth Creation

Tax planning should not focus only on tax savings.

Tax-efficient investments help create wealth while reducing tax liability.

Examples include:

- Equity Linked Savings Schemes (ELSS)

- National Pension System (NPS)

- Public Provident Fund (PPF)

- Retirement plans

These investments offer both tax and financial benefits.

4. Use Health Insurance Benefits

Health insurance provides financial protection and tax benefits.

Premiums paid for eligible policies can qualify for deductions under applicable provisions.

Benefits include:

- Reduced taxable income

- Medical risk protection

- Long-term financial security

5. Plan Capital Gains Carefully

Investors often overlook tax planning opportunities related to capital gains.

Proper planning can help:

- Reduce tax liability

- Optimize investment returns

- Manage gains efficiently

Investors should maintain accurate records of:

- Purchase dates

- Sale dates

- Acquisition costs

6. Separate Personal and Business Expenses

Freelancers and business owners should maintain separate financial records.

This helps:

- Track expenses accurately

- Claim eligible deductions

- Simplify compliance

Mixing expenses often results in missed deductions and accounting difficulties.

7. Maintain Proper Financial Records

Good record keeping supports better tax planning.

Important documents include:

- Salary statements

- Bank statements

- Investment records

- Property documents

- Expense invoices

Organized records simplify filing and improve compliance accuracy.

Tax Planning for Salaried Employees

Salaried taxpayers can benefit from:

- HRA optimization

- Retirement planning

- Health insurance deductions

- Tax-saving investments

- Capital gains management

Proper planning helps maximize take-home income.

Tax Planning for Freelancers

Freelancers often have:

- Multiple income sources

- Business expenses

- Advance tax obligations

Tax planning helps:

- Track deductible expenses

- Improve compliance

- Reduce taxable income legally

Tax Planning for Business Owners

Business owners face additional tax obligations, including:

- Income Tax

- GST

- TDS

- Payroll taxes

Strategic planning helps optimize business finances and improve profitability.

Common Tax Planning Mistakes

Many taxpayers make avoidable mistakes such as:

Waiting Until Year-End

Last-minute planning limits available options.

Missing Deductions

Failure to track eligible expenses often increases tax liability.

Ignoring Tax Regime Comparison

Choosing the wrong regime may result in higher taxes.

Poor Documentation

Incomplete records can create compliance problems.

Not Seeking Professional Advice

Tax laws change regularly and may affect planning decisions.

Benefits of Professional Tax Planning

Professional tax advisors help taxpayers:

- Reduce tax liability legally

- Identify deductions

- Compare tax regimes

- Improve compliance

- Plan investments efficiently

Expert guidance often produces significant financial benefits.

Why Choose Easy Tax?

Easy Tax provides professional tax planning and filing services for individuals and businesses across India.

Our Services Include

- Income Tax Return Filing

- Tax Planning

- GST Advisory

- TDS Compliance

- NRI Taxation

- Business Tax Consultation

- Financial Advisory Services

Why Clients Choose Easy Tax

- Experienced tax professionals

- Personalized tax strategies

- Affordable pricing

- Fast online support

- Accurate compliance assistance

We help clients simplify taxes and maximize financial efficiency.

Frequently Asked Questions (FAQs)

What are income tax slabs?

Income tax slabs are income ranges used to determine the tax rates applicable to different portions of income.

Does entering a higher tax slab increase tax on all income?

No. Only the portion of income exceeding the slab threshold is taxed at the higher rate.

How can I legally reduce my tax liability?

You can reduce taxes through deductions, exemptions, tax-efficient investments, and proper financial planning.

Which tax regime is better?

The best regime depends on your income, deductions, investments, and financial situation.

Do freelancers need tax planning?

Yes. Freelancers often benefit significantly from expense deductions and structured financial planning.

Can Easy Tax help with tax planning?

Yes. Easy Tax provides tax planning, filing, compliance, and advisory services tailored to individual and business needs.

Final Thoughts

Understanding income tax slabs is one of the most important steps toward effective tax management. When taxpayers understand how taxes are calculated and how deductions, exemptions, and investment strategies affect taxable income, they can make smarter financial decisions and reduce their tax burden legally.

Whether you are a salaried employee, freelancer, investor, startup founder, or business owner, proactive tax planning can improve savings, strengthen compliance, and support long-term financial growth.

With expert guidance from Easy Tax, taxpayers can navigate complex tax regulations confidently while maximizing available tax-saving opportunities and building a stronger financial future.