Written and reviewed by CA Pritam Sharma | Updated: July 2026 | EasyTax Global IT Solutions Pvt. Ltd.

Quick Answer

Form GST RFD-02 is the acknowledgement issued against your GST refund application (RFD-01). Issued under Rules 90(1), 90(2) and 95(2) of the CGST Rules, 2017, it confirms the proper officer has found your application complete and has taken it up for processing. It must be issued within 15 days of filing, is system-generated and requires no signature.

Important: RFD-02 is not a sanction. Your refund is not approved. It means your application was not defective — the opposite outcome is RFD-03, a deficiency memo, which forces you to file a fresh application.

Every exporter and every business sitting on an inverted duty structure knows the wait. You file the refund, and then nothing — until an email arrives with an acknowledgement number attached. That email is RFD-02, and most claimants misread what it means.

This guide explains what RFD-02 actually confirms, the legal clock it starts, how it differs from RFD-03, where to download it, and what to do when it does not arrive.

What Is Form GST RFD-02?

RFD-02 is the Acknowledgement in the GST refund series. When you submit Form GST RFD-01 on the portal, the proper officer scrutinises it for completeness — not for merit. If the application and its annexures are in order, an acknowledgement in Form GST RFD-02 is issued electronically, communicating that the claim has been accepted for processing.

The rule references printed on the form tell you its scope:

- Rule 90(1) — refund claims filed under Rule 89(1), i.e. the standard refund route.

- Rule 90(2) — all other refund applications, after scrutiny for completeness within 15 days.

- Rule 95(2) — refunds to UN bodies, embassies and notified agencies claiming under Form GST RFD-10.

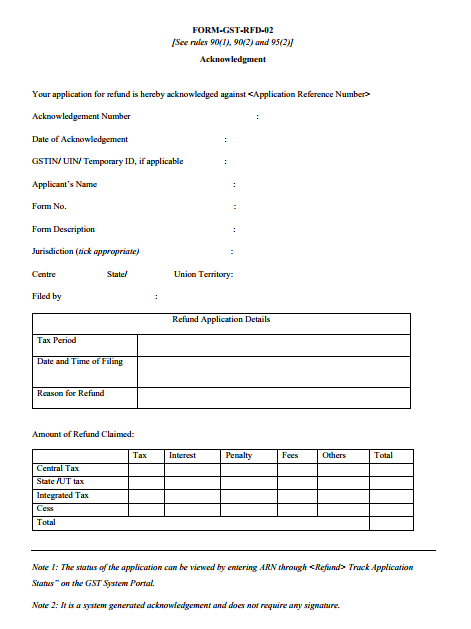

Format of Form GST RFD-02

The form opens with a single line: "Your application for refund is hereby acknowledged against <Application Reference Number>." Read that sentence literally. It acknowledges. It does not sanction.

The fields it carries:

| Field | What It Records |

|---|---|

| Acknowledgement Number | Unique reference for this acknowledgement |

| Date of Acknowledgement | Date the officer accepted the claim for processing |

| GSTIN / UIN / Temporary ID | Identity of the claimant |

| Applicant's Name | Legal name as registered |

| Form No. and Description | The refund form being acknowledged (RFD-01 or RFD-10) |

| Jurisdiction | Centre / State / Union Territory — tick appropriate |

| Filed by | Authorised signatory who submitted the claim |

| Refund Application Details | Tax period, date and time of filing, reason for refund |

| Amount of Refund Claimed | Central Tax, State/UT Tax, Integrated Tax and Cess — split across Tax, Interest, Penalty, Fees and Others |

Two notes are printed at the foot of the form, and both matter. Note 1: status is trackable by entering the ARN under Refunds > Track Application Status on the GST portal. Note 2: it is a system-generated acknowledgement and does not require any signature — so an unsigned RFD-02 is not defective, and nobody needs to chase a stamp.

Check the Amount of Refund Claimed table against what you actually filed. If the figures differ from your RFD-01, raise it immediately rather than at the sanction stage.

The Clock RFD-02 Starts — and the One It Does Not

This is the most commercially valuable paragraph on this page.

Under Section 54(7), the proper officer must issue the final refund order within 60 days from the date of receipt of a complete application. Under Section 56, if the refund is not paid within those 60 days, interest at 6% per annum becomes payable — rising to 9% where the refund arises from an order of an appellate authority, tribunal or court and is delayed beyond 60 days from the application following that order.

The critical detail: the 60-day clock runs from the date of filing the application, not the date of the acknowledgement. RFD-02 records that filing date precisely so it cannot be disputed later. When a deficiency memo intervenes and you file afresh, the clock generally restarts from the fresh filing — which is exactly why a deficiency memo is expensive.

Keep every RFD-02. If a refund runs long, that form is your primary evidence of when the clock started.

RFD-02 vs RFD-03: The Fork in the Road

Within 15 days of filing, exactly one of two things arrives.

| RFD-02 (Acknowledgement) | RFD-03 (Deficiency Memo) | |

|---|---|---|

| Meaning | Application complete, taken up | Application defective |

| Rule | Rule 90(1) / 90(2) / 95(2) | Rule 90(3) |

| What happens next | Officer proceeds to examine merits | You must file a fresh RFD-01 |

| Credit ledger | Debited amount stays blocked | Debited ITC is re-credited |

| Effect on 60-day clock | Runs from original filing | Restarts on the fresh application |

Per CBIC Circular 125/44/2019, only one deficiency memo may be issued per refund application — an officer cannot drip-feed objections across successive memos. The rectified application must nonetheless be filed within the two-year limitation from the relevant date under Section 54(1), which has been the source of considerable litigation where the memo landed close to the deadline.

Got an RFD-03 instead of an RFD-02?

We diagnose the deficiency, fix the annexures and refile before your limitation window closes — and follow the claim through to sanction.

Where RFD-02 Sits in the GST Refund Process

| Form | Purpose | Issued By |

|---|---|---|

| RFD-01 | Refund application | Taxpayer |

| RFD-02 | Acknowledgement | Proper officer / system |

| RFD-03 | Deficiency memo | Proper officer |

| RFD-04 | Provisional refund order — 90% for zero-rated claims | Proper officer |

| RFD-05 | Payment advice | Proper officer |

| RFD-06 | Final sanction or rejection order | Proper officer |

| RFD-07 / 08 / 09 | Withholding order / SCN / reply to SCN | Officer & taxpayer |

| RFD-10 / RFD-11 | Refund for UN bodies & embassies / LUT for exports | Taxpayer |

For zero-rated exporters, RFD-02 has a second consequence: it triggers the RFD-04 provisional refund of 90%, which under Rule 91 should follow within 7 days of the acknowledgement. No RFD-02, no provisional refund.

RFD-02 Download: Where to Find It

RFD-02 is delivered to your registered email and flagged by SMS. To retrieve it from the portal — the infrastructure for all of this is run by GSTN:

- Log in at gst.gov.in.

- Go to Services > Refunds > Track Application Status and enter your ARN.

- Alternatively use Services > User Services > View Notices and Orders.

- Open the acknowledgement and download the PDF. No signature or DSC verification is needed.

There is no blank "RFD-02 download" for taxpayers to fill in. The form is issued to you, never by you. If a search result offers an editable RFD-02 template, it is describing the CBIC format, not something you file.

What If RFD-02 Never Arrives?

Rule 90 gives the officer 15 days. In practice, silence past that window usually means one of four things:

- The ARN never generated — the application was saved, not submitted. Check the ARN first, before anything else.

- Jurisdiction mismatch — the claim is sitting in the wrong officer's queue between Centre and State.

- Statement mismatch — the annexure does not reconcile with your GSTR-1, GSTR-3B or GSTR-2B. This is the most common cause and the one you can prevent.

- Shipping bill / e-invoice mismatch — export data from ICEGATE or the e-invoice portal does not align with the return.

Escalate through the portal grievance facility with your ARN, then to the jurisdictional office. Reconciliation done before filing prevents most of this — clean GST returns are the real precondition for a fast refund, and annual reconciliation via GSTR-9C, prepared using the GSTR-9C offline utility, surfaces the gaps that stall claims.

Frequently Asked Questions

What is RFD-02 in GST?

Form GST RFD-02 is the acknowledgement issued against a GST refund application under Rules 90(1), 90(2) and 95(2) of the CGST Rules, 2017. It confirms the application has been found complete and taken up for processing, and records the ARN, filing date and amount claimed.

Does RFD-02 mean my refund is approved?

No. RFD-02 acknowledges only that the application is complete. The refund may still be sanctioned in full, sanctioned in part, or rejected. Sanction or rejection is communicated separately in Form GST RFD-06.

Within how many days is RFD-02 issued?

Within 15 days of filing the refund application, as prescribed by Rule 90. If the application is deficient, a deficiency memo in Form GST RFD-03 is issued within the same 15-day period instead.

Does RFD-02 need to be signed?

No. The form states expressly that it is a system-generated acknowledgement and does not require any signature. An unsigned RFD-02 is perfectly valid.

How do I download RFD-02?

Log in to gst.gov.in and go to Services > Refunds > Track Application Status, enter your ARN, and download the acknowledgement. It is also available under Services > User Services > View Notices and Orders, and is emailed to your registered address.

What is the difference between RFD-02 and RFD-03?

RFD-02 is an acknowledgement of a complete application. RFD-03 is a deficiency memo issued under Rule 90(3) when the application is defective — it re-credits the debited ITC and requires you to file a fresh refund application after rectification.

Do I get interest if my refund is delayed after RFD-02?

Yes. Under Section 56, interest at 6% per annum is payable if the refund is not paid within 60 days from the date of receipt of the application, and 9% where the refund arises from an appellate or court order and is similarly delayed.

Conclusion

RFD-02 is a small form doing quiet, important work. It is not your refund and it is not an approval — it is proof that your claim was filed properly, on a specific date, for a specific amount, and that the statutory clock is running. Read it against your RFD-01, keep it filed, and treat its absence past 15 days as a signal rather than an inconvenience.

The best refund strategy is upstream of the form entirely: reconcile before you file, so RFD-02 arrives instead of RFD-03. For the wider framework, see our GST law in India guide 2026, and track changes through the GST notifications summary and latest GST news updates — refund circulars change more often than the rules do. New registrants should start with the GST registration documents checklist.

GST Refunds, Handled End to End

Export refunds, inverted duty structure claims, deficiency memos and delayed-interest follow-ups — managed by chartered accountants. From Bhamashah Techno Hub, Jaipur, for businesses across India.

Disclaimer: This article is for educational purposes and does not constitute legal or tax advice. GST rules, circulars and portal workflows change frequently; positions stated are as understood at the time of writing. The form image is the CBIC-prescribed format reproduced for reference. Please verify current requirements on gst.gov.in or consult a qualified professional before acting.